UK Inflation & Wages Keep the Bank of England on its Rate Hiking Path

Elevated Inflation

Households in the UK face a very high cost of living, as a result of the monetary and fiscal stimulus to alleviate the economic impact of the Covid-19 pandemic, the effects of the war in Ukraine that sent food and energy prices higher and other factors.

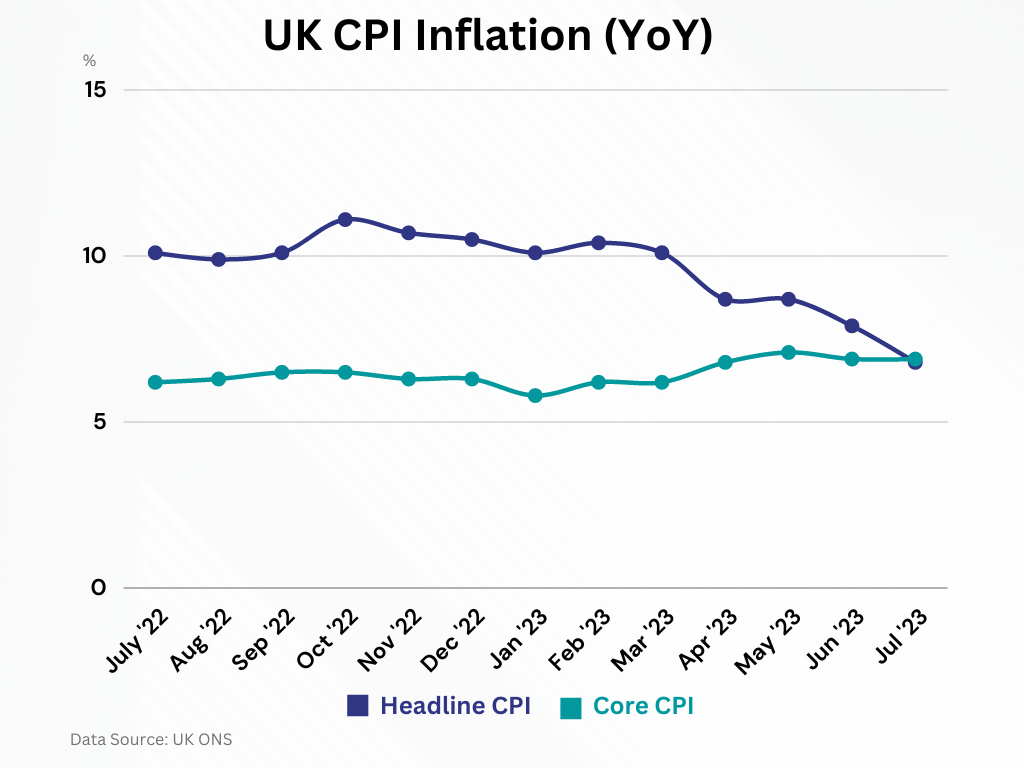

The Consumer Price Index (CPI) peaked at an eye-watering 11.1% in October 2022, which is the highest level since at least 1997, when the national statistics series began [1]. Since then, there has been progress, with this week's data showing that headline inflation moderated to 6.8% y/y in July, in the smallest increase in more than a year.

On the other hand, Core inflation that excludes food, energy, alcohol and tobacco prices has been accelerating this year, hitting 7.1% y/y in May and the highest level in thirty-one years. It did ease though from its peak over the last two months, to 6.9% y/y.

The last two CPI reports, offered a glimmer of hope since they showed a moderation in price pressures and the Bank of England expects inflation to "fall significantly further". However, it is still very high and policymakers don't expect it to fall below the 2% target before Q2 2025. [2]

High Wages

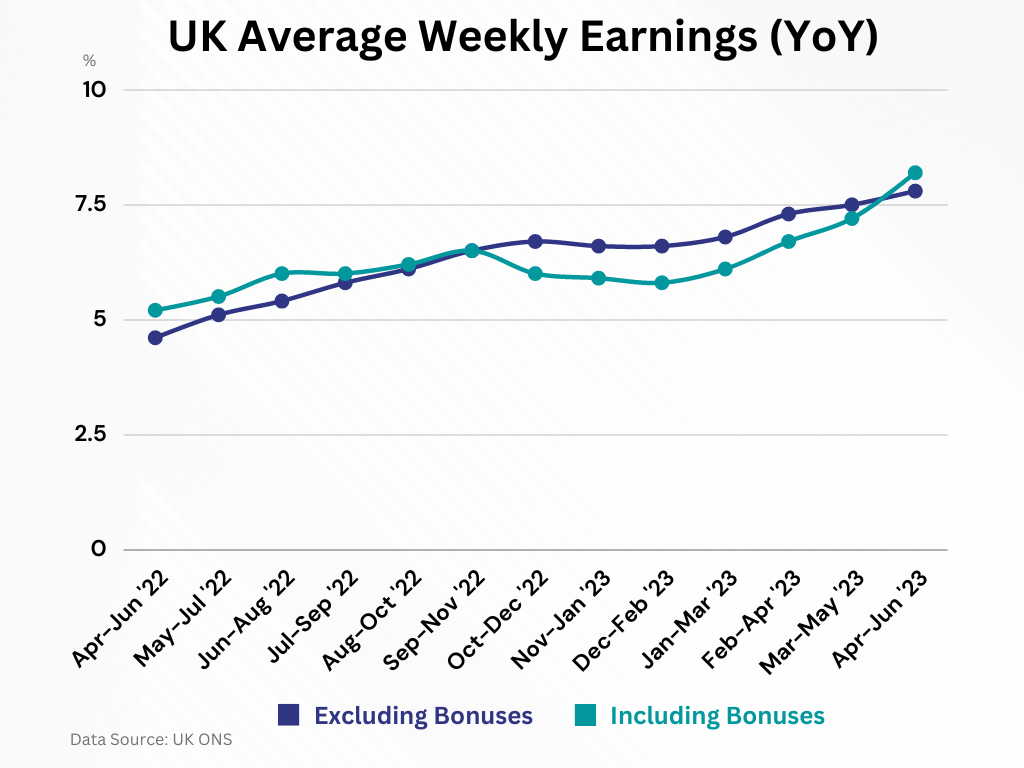

At the same time, the labor market "remains tight", despite some signs of easing. According to Tuesday's release, Unemployment increased to 4.2% y/y in the April June period, but wages rose further to new historical highs. Excluding bonuses, average hourly earnings of 7.8% y/y marked the biggest increase since 2001, when "comparable records began" [3]. Total pay of 8.2% y/y was the highest in roughly two years.

This is a constant headache for the central bank, since it makes the job of lowering inflation harder and feeds a wage-price spiral. The BoE alluded to such second-round effects this month, which it believes are "likely to take longer to unwind than they did to emerge" [2]. Furthermore, Governor Bailey has repeatedly stressed that the elevated wages are "not consistent with the inflation target". [4]

More Tightening in Play

In order to bring consumer prices down, the Bank of England started raising interest rates all the way back in December 2021, much earlier than its major counterparts. However, it squandered the first part with small hikes, in an approach that clearly did not work, since inflation repeatedly surprised to the upside.

Although it has been coming down, inflation remains elevated and is not projected to hit the 2% target for another two years. The combination with historically high wage growth, puts pressure on the central bank to deliver more hikes and maintain a prolonged restrictive stance. Furthermore, the forecasts are conditioned on rates rising to "a peak of just over 6%", from current 5.25%, which shows that more tightening is likely. [2]

Reasons for Restrain

Despite the seemingly reluctant stance for a large part of its tightening cycle, the BoE has delivered a sizeable amount of firming since the 2021 lift-off, worth 515 basis points. Its actions sent borrowing costs higher, with the two-year bond yields surpassing the September 2022 peak of the mini-budget debacle that eventually led then PM Truss to step down.

The massive amount of tightening stresses households and business, pushing mortgage costs higher. In its Q2 Financial Stability Report, the BOE estimating that a typical mortgagor would see the interest rates payment increase by £220 over the second half of the year, when rolling over a fixed-rate deal. [5]

It also creates risk for an overall protracted economic slowdown. Although the UK economy has generally performed better than expected and the BoE does not anticipate a recession anymore, it actually lowed its GDP growth forecasts for the next two years.

Uncertain Outlook

Global monetary policy has entered an intricate phase where banks have become increasingly data-dependent and unwilling to provide forward guidance, creating an uncertain outlook. The Bank of England has been a usual suspect in terms of vague communication and its latest policy decision reaffirmed its non-committal stance.

It offered no insights as to the next steps after raising rates by 0.25% in august, in a three-way split decision that only added to the uncertainty. It kept the door open to more moves, but did not commit to any and kept its option open.

With high inflation and wage growth, it is hard to see officials backing down. On the other hand, they may need to tread carefully, since in their effort to mitigate the high cost of living crisis they risk triggering a borrowing crisis.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. He has a long time presence at FXCM, as he joined the company in 2011. He has served from multiple positions, but specializes in financial market analysis and commentary.

With his educational background in international relations, he emphasizes not only on Technical Analysis but also in Fundamental Analysis and Geopolitics – which have been having increasing impact on financial markets. He has longtime experience in market analysis and as a host of educational trading courses via online and in-person sessions and conferences.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.