RBA Stood Pat on Rates Again but Kept More Tightening In Play

RBA Stood Pat, More Hikes Not Ruled Out

The Reserve Bank of Australia has made significant progress in cooling price pressures, since the Consumer Price Index moderated to 4.1% in Q4. Furthermore, the economy has been facing headwinds and grew by just 0.2% q/q in Q3, marking the slowest pace in two years. Labor market conditions are easing, with the last report revealing the loss of 65,100 jobs in December and the worst since September 2021.

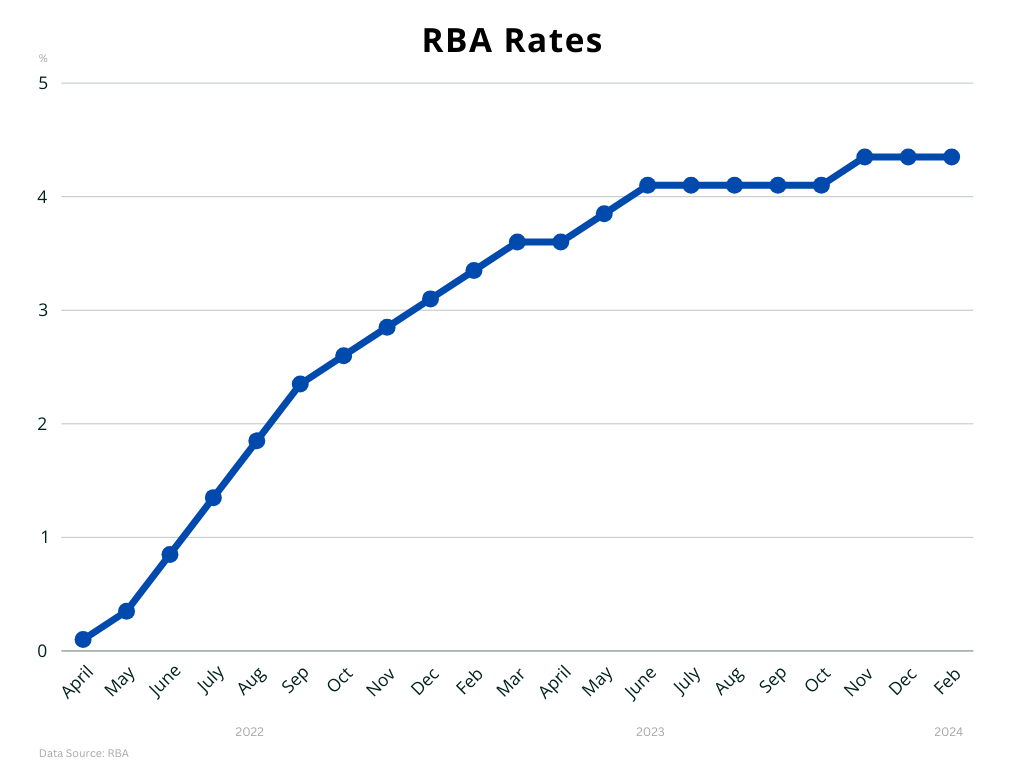

The central bank has produced 425 basis points of tightening since the May 2022 lift-off, in order to bring down inflation. Given the cumulative tightening, the lags in the transmission mechanism and the above economic data, policymakers decided on Tuesday to keep rates unchanged at 4.35% for second straight time. [1]

They acknowledged the easing of inflation and expect it to return to the 2-3% goal by the end of 2025, lowering their projections through the forecast period. These projections are conditioned on market pricing that rates have peaked and will be lowered in the second half of the year. [2]

However, the labor market is "tighter" than what would be consistent with the RBA's mandate, wage growth is elevated and inflation"remains high". Echoing their US peers, officials noted that they "need to be confident" inflation is moving "sustainably" towards the target range. Going a step further, they stressed that "a further increase in interest rates cannot be ruled out". During her press conference, Governor Bullock warned that officials have "more work to do" and "a little way to go" to get inflation down. [3]

The Reserve Bank of Australia is at an intricate phase and has adopted a non-committal stance, having already delivered a significant amount of tightening. Lower inflation, a labor market that is coming into better balance and economic headwinds, point to peak rates and eventually cuts, which is what markets are pricing. On the other hand, policymakers don't expect inflation to return to target for nearly two more years, which leads them to keep hikes on the table and makes any cut talk premature.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. He has a long time presence at FXCM, as he joined the company in 2011. He has served from multiple positions, but specializes in financial market analysis and commentary.

With his educational background in international relations, he emphasizes not only on Technical Analysis but also in Fundamental Analysis and Geopolitics – which have been having increasing impact on financial markets. He has longtime experience in market analysis and as a host of educational trading courses via online and in-person sessions and conferences.

References

| Retrieved 06 Feb 2024 https://www.rba.gov.au/media-releases/2024/mr-24-01.html | |

| Retrieved 06 Feb 2024 https://www.rba.gov.au/publications/smp/2024/feb/pdf/statement-on-monetary-policy-2024-02.pdf | |

| Retrieved 27 Apr 2024 https://rba.livecrowdevents.tv/MediaConferenceMonetaryPolicyDecision6feb/stream |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.