Non-Committal Central Banks Set the Stage for an Uncertain Autumn

Messy Monetary Landscape

Most major central banks have been hiking rates for the past several months in order to mitigate surging inflation, which was a result of the pandemic stimulus, soaring energy prices from the war in Ukraine and other factors. This tightening cycle started in late-2021, with the Reserve Bank of New Zealand (RBNZ) and heated up in the past year, as more banks entered the hawkish arena.

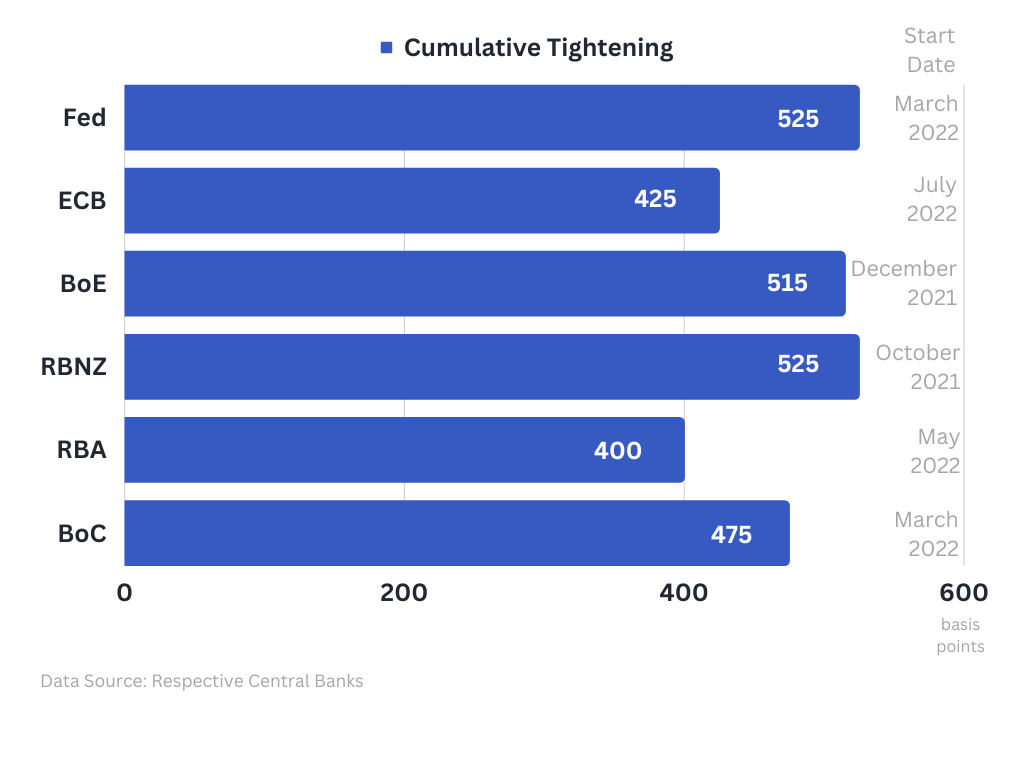

Although not in total sync, most of those central banks have been on the same page up until recently, implementing historically aggressive rate increases. The US Fed and the RBNZ are the most hawkish, having delivered 525 basis points of hikes each, since their respective lift-offs. As of the time of writing, this is the cumulative tightening and start dates:

During the current year however, CBs have been slowing down and diverging, as their actions affect the domestic economies in varying degrees and as they approach the end of the tightening cycles (if not already there). Many of them have paused and restarted and intra-bank cohesion has eroded, in an overall messy monetary environment.

As the latest round of decisions showed, policymakers are increasingly more data-driven and also unwilling to provide explicit forward guidance, creating high uncertainty around the monetary policy outlook at a crucial junction.

US Fed

Following a timid start, the US central bank became very aggressive, but has slowed the pace of firming this year, as it comes closer to (or is at) the terminal rate. Officials hit the pause button in June, after ten consecutive moves, but raised rates again in July.

Inflation has been coming down and the last PCE report was encouraging, as headline decelerated to 3% y/y in June, while the stickier core also eased notably to 4.1% y/y. Despite some indications of cooling, the labor market remains tight with elevated wages and unemployment close to its five-decade lows. At the same time, the economy continues to perform better than expected.

Given the inflation moderation, as well as the cumulative tightening and its lagging nature, the Fed may have already done enough to bring inflation to the 2% target. However, achieving this goal without a significant negative impact to the labor market and economic activity would defy the Phillips curve.

The Fed finds itself once again being pulled to different directions, so it's no surprise that Chair Powell refrained from any guidance as to the next moves. He said that both a pause and a hike are possible in September, adding to the uncertainty. The last projections imply an additional 25 basis points of hikes this year, but markets never embraced that and believe that the terminal rate has already been reached.

European Central Bank

The ECB was a laggard on the tightening front, having started hiking rates later than its major counterparts and from a lower point. Despite the late entry, it quickly delivered outsized increases and has maintained a very hawkish stance.

Policymakers did raise rates by another 0.25% in July, but the outlook is now murky. This time around, President Lagarde adopted an ambiguous stance around the next steps, echoing her US peer. In stark contrast with her recent hawkish press conferences, she said that "we might hike and we might hold" and when asked if there is there is more work in raising rates, her reply was: "At this point in time, I wouldn't say so". [1]

The truth is that the ECB has a tough job and there is a slew of data to assess until the next meeting. Headline inflation is coming down, but is still far from the 2% target, while core has been particularly persistent. At the same time, the economic engine of Eurozone is sputtering, since Germany is in a technical recession, with two straight negative quarters. Eurozone has avoided that so far and preliminary Q2 GDP showed 0.3% expansion, creating hopes for a soft landing.

This was the first time Ms Lagarde opened the door to a hold, but delivering such an outcome may be harder than it sounds, since there is more work needed on inflation. Even if the ECB pauses in September though, it does not mean that rates have peaked, adding to the perplexity.

Bank of England

The BoE squandered the initial part of its tightening cycle with small hikes, before picking up speed. It found itself in the same position again earlier in the year, as it appeared to be hiking rates reluctantly. This approach clearly did not work, since inflation repeatedly surprised to the upside.

Policymakers were forced to reaccelerate in July with an 0.5% move, but climbed down in August, to a miniscule 25 basis point increase. The stubborn core inflation ticked down in June and headline decelerated further, allowing them this less aggressive action.

However, inflation remains far from the 2% target and the bank does not expect a fall below it before Q2 2025. Furthermore, the labor market is very hot and wages at historic highs, making the situation worst. Given these factors, it is hard to see how officials can stop here. Having said that, they may need to tread carefully given growing fears around the impact to the economy, the housing market and mortgages, which pressure households and businesses.

The Bank of England is a serial offender in terms of poor communication and vague guidance and things have only gotten worse, as it has now entered into a restrictive monetary stance. What's more, divisions amongst policymakers have been constant and the last three-way split decision is a testament to that. As such, there is great uncertainty in regards to the policy path from here.

Reserve Bank of New Zealand

The RBNZ has been consistently aggressive since the October 2021 lift-off, with a relentless tightening pace, which produced 525 basis points of hikes in twelve straight meetings. Things changed in July though, as policymakers decided to keep rates unchanged, in watershed decision for one of the most hawkish central banks and held rates at 5.5% again in August. In an interesting twist though, they upgraded their terminal OCR forecast to 5.6% for 2024, leaving the door open to further tightening.[2]

The cumulative tightening is having an impact, sending the economy into a technical recession and the bank expects two more quarters of contraction, while Inflation is moderating. At 6% y/y in Q2 however, headline CPI has a long way to go until it falls to the 1-3% target. Furthermore, the labor market is very tight and wages at historical highs, despite signs of easing.

Given the above, officials may have a hard time not hiking again, at a time when many of their peers have overestimated the inflation progress and have been forced to restart or reaccelerate their tightening programs.

Reserve Bank of Australia

The central bank of Australia has a had a few back and forths this year, making its monetary firming program somewhat messy. After a brief pause earlier in 2023, it delivered two straight hikes and then stayed in the sidelines again in July and August.

Its actions are having an impact on inflation with headline CPI moderating further in Q2 to 6% y/y and this could allow them to stand pat again in September. In spite of that, policymakers kept the door open to more moves and it is hard to say that the end of the road has been reached.

Inflation is still elevated and not projected to fall within the 2-3% target before late-2025. At the same time, the labor market is very tight, despite some signs of easing.

Bank of Canada

The Bank of Canada has delivered jumbo hikes, going as high as a full percentage point in July of the past year, but was also the first major central bank to hit the pause button this March. After standing pat in the two meetings that followed, it changed tacked. It raised rate in June after being spooked in by an inflation uptick and doubled down in July with another move. [3]

Policymakers abstained from offering forward guidance, which makes it hard to assess the future policy path. However, it is likely that they have not reached the end of the road, since they expressed concerns that inflation progress toward the 2% target "could stall". Moreover, they raised their CPI forecast for this year and the next.

Bank of Japan

The BoJ is on the other end of the policy spectrum, with an ultra easy stance, having struggled with deflation for decades. This makes it reluctant to change its ways, even though inflation has been printing above the 2% target for nearly a year and officials raised their median projection to 2.5% for FY2023. [4]

Speculation around an exit from the uber-dovish policies has been mounting after the bank had opened the door, with the widening of its yield curve control (YCC) to +/-0.5% back in December of 2022. Last month, it kept the range in place, but effectively widened the YCC by offering to buy 10-year JGBs at 1%.

In theory, this is another step towards normalization, but it also facilitates the continuation of the loose monetary stance. The already perplexed situation is aggravated by the implicit nature of the YCC tweak, which makes the bank's policy even more unconventional.

It is clear that policymakers did not want to commit too much to a higher yield range and that they are not yet ready to normalise policy. On the other hand, the stark policy differential with its peers, has been detrimental to the Yen. Authorities were forced to step in the FX market last year to contain the USD/JPY rally and we are seeing renewed verbal interventions.

Uncertain Outlook

Monetary policy has been all-over the place this year and has now entered a crucial juncture. Central banks have already delivered a massive amount of tightening and inflation is generally decelerating. This creates an inclination to stop, given also the lagging nature of the transmission mechanismm, but they are reluctant to call it a day. Many of them have overestimated the inflation progress in the past, whereas strong labor markets call for sustained restrictive stance.

We are now at an intricate and nuanced phase of monetary policy, where every data point matters and there is a large number of them until the next round of meetings. Policymakers have repeatedly stressed that they will be driven by the data. This also creates intra-bank divisions and make them unwilling and unable to provide forward guidance, keeping all options on the table.

This non-committal stance makes the policy outlook unclear and sets the stage for an uncertain autumn. This enhanced unpredictability can make markets jittery and be a source of volatility. Wall Street has rallied this year due to the AI boom and expectations for an end to the Fed's hiking cycle. Can it go on though, if those hopes don't materialize? EUR/USD is up on the year, due to the more aggressive ECB stance, but can it push higher with a September pause now on the table? USD/JPY has rallied again in 2023, due to the favorable policy differential, but if the Fed reaches the terminal rate and the BoJ eventually starts a normalization process, there is potential for significant repricing.

This article was updated on August 17, to reflect the latest policy decision by the RBNZ

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. He has a long time presence at FXCM, as he joined the company in 2011. He has served from multiple positions, but specializes in financial market analysis and commentary.

With his educational background in international relations, he emphasizes not only on Technical Analysis but also in Fundamental Analysis and Geopolitics – which have been having increasing impact on financial markets. He has longtime experience in market analysis and as a host of educational trading courses via online and in-person sessions and conferences.

References

| Retrieved 04 Aug 2023 https://www.ecb.europa.eu/press/pressconf/2023/html/ecb.is230727~e0a11feb2e.en.html | |

| Retrieved 04 Aug 2023 https://www.rbnz.govt.nz/hub/-/media/project/sites/rbnz/files/publications/monetary-policy-statements/2023/august/mpsaug23.pdf | |

| Retrieved 04 Aug 2023 https://www.bankofcanada.ca/2023/07/fad-press-release-2023-07-12/ | |

| Retrieved 02 May 2024 https://www.boj.or.jp/en/mopo/outlook/gor2307a.pdf |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.