USD/JPY Mixed as Japan Inflation Soars above BoJ’s Target, Putting Pressure for a Policy Shift

Japan's Inflation Surged

Japan's Consumer Price Index (CPI) excluding fresh food, jumped 2.1% in April year-over-year from 0.8% prior, marking the highest level since March 2015.

It is also higher than the central bank's 1.9% median forecast for the current fiscal year [1] and has now surpassed the BoJ's 2% target.

Headline CPI rose to seven-year highs as well, coming in at 2.5% year-over-year from 1.2% in the previous month, while CPI less fresh food and energy prices surged 0.8% year-over-year from -0.7% prior.

These latest inflation figures come just two days after the Gross Domestic Product (GDP) data, which showed that the Japanese economy contracted by 1% in the first quarter of the year (annualized).

Dovish Bank of Japan (BoJ)

The country's central bank is in the far dovish side of the monetary policy spectrum, in stark contrast with its major counterparts.

In its last policy meeting in late April, it maintained interest rates at -0.1% and said it will continue its ultra-loose policy, in order to achieve the price stability target of 2% and as long as necessary for "maintaining that target in a stable manner". [2]

The Bank of Japan (BoJ) has also been stepping in to the bond market and had reiterated its pledge to buy limitless amount of government bonds (JGBs), so that the 10-year yield will remain at around zero percent, adding that it will offer to purchase 10-year JGBs at 0.25% on every business day.

The Summary of Opinions from that meeting which was published last week, reaffirmed the BoJ's uber-dovishness, since it revealed that officials viewed as "necessary" the continuation of the current "powerful monetary easing". [3]

Fed-BoJ Policy Differential

Given that the Bank of Australia hiked rates for the first time in more than 10 years earlier in the month and that the European Central Bank has been increasingly hawkish, with some officials seeing rate hikes as early as July, the policy differential between the Fed and the BoJ is now the most pronounced one among major central banks.

But could this start to change? Fed Chair Powell reasserted the bank's hawkishness and its commitment to bring inflation down this week [4], but the next interest rate adjustments are well-telegraphed and relatively timid, since he had essentially ruled out larger 75 basis points hikes during his last press conference [5].

Furthermore, US GDP contracted by 1.4% in the first quarter (annualized), initial jobless claims increased last week to 218K and inflation remains elevated, despite April's moderation. The Fed's tightening actions could aggravate the economic situation and perhaps make it more conservative in order to avoid a hard landing.

With inflation now having unexpectedly surpassed its 2% target and its loose monetary policies and yield curve control harming the Yen, the Bank of Japan may be forced to rethink its extremely dovish monetary strategy.

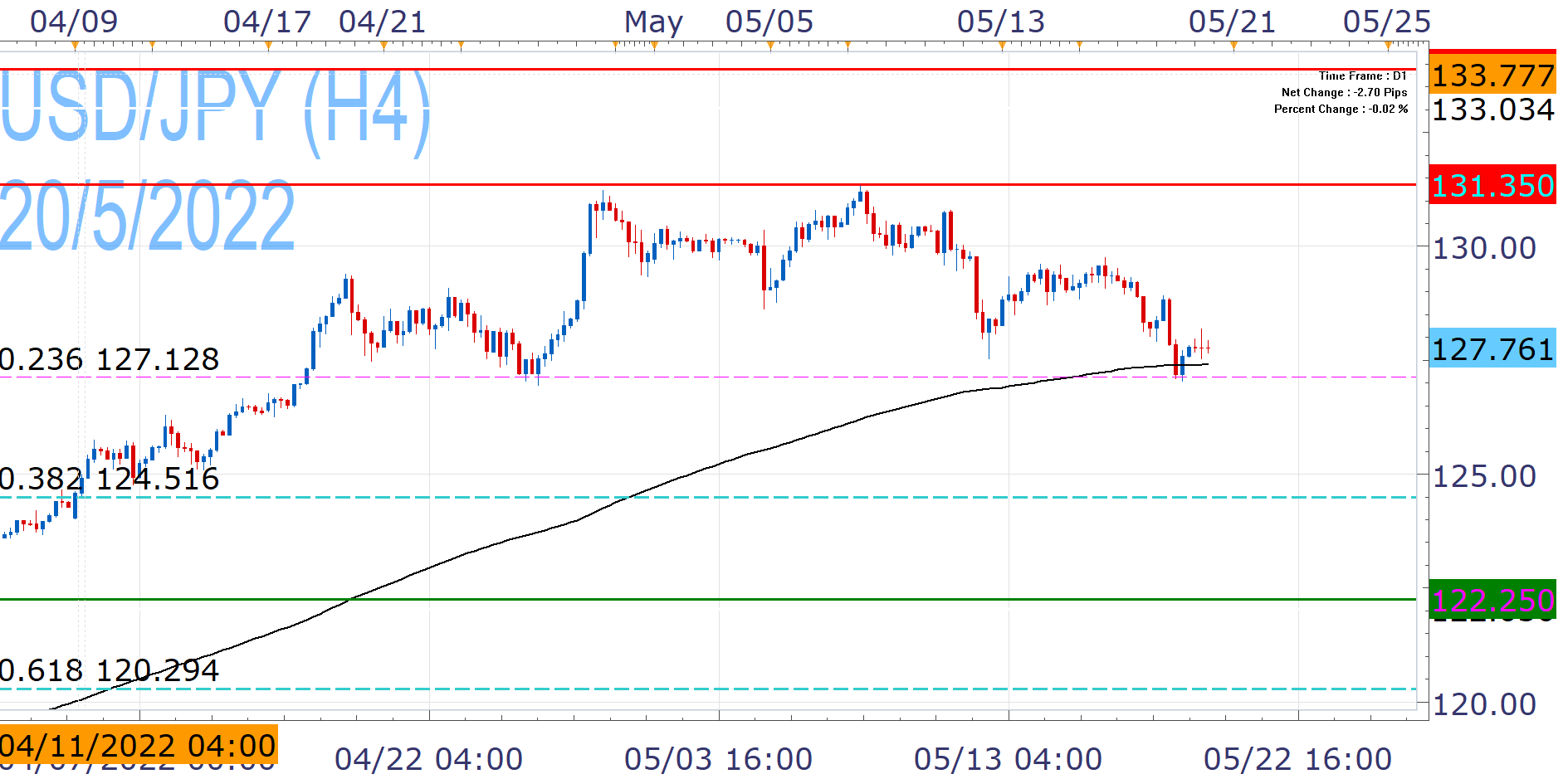

USD/JPY Analysis

This monetary policy divergence has propelled the pair into a massive nine-week rally, which culminated to a 20+ years high (131.35).

However, the Fed's recent "conservatism" has allowed the Yen to snap the aforementioned streak and rekindle its safe-haven appeal, as fears of stagflation intensified this week, following the poor quarterly results from major US retailers.

USD/JPY heads towards its second straight losing week, having tested yesterday key EMA200 (black line) and 23.6% Fibonacci from this year's lows to the highs, as we had warned from our last analysis.

A successful break below this area would pause the upwards momentum and open the door to a correction towards the 38.2% Fibonacci (124.51), but it would be a stretch for now to talk a about a larger decline to 122.25.

Despite the recent weakness, the greenback has managed to defend the above key levels two times, avoiding a close below them yesterday. This can give it the chance to rebound towards 129.77, although under these conditions, fresh 20-year highs (131.35) may not come easy.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. He has a long time presence at FXCM, as he joined the company in 2011. He has served from multiple positions, but specializes in financial market analysis and commentary.

With his educational background in international relations, he emphasizes not only on Technical Analysis but also in Fundamental Analysis and Geopolitics – which have been having increasing impact on financial markets. He has longtime experience in market analysis and as a host of educational trading courses via online and in-person sessions and conferences.

References

| Retrieved 20 May 2022 https://www.boj.or.jp/en/mopo/outlook/gor2204a.pdf | |

| Retrieved 20 May 2022 https://www.boj.or.jp/en/announcements/release_2022/k220428a.pdf | |

| Retrieved 20 May 2022 https://www.boj.or.jp/en/mopo/mpmsche_minu/opinion_2022/opi220428.pdf | |

| Retrieved 20 May 2022 https://www.youtube.com/watch | |

| Retrieved 26 Apr 2024 https://www.federalreserve.gov/monetarypolicy/fomcpresconf20220504.htm |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.