Netflix Hikes Prices as Revenue & Subs Growth Accelerated in Q3 2023

Key Takeaways

-The streaming giant reported overall strong Q3 results on Wednesday October 18, beating estimates

-The results were driven largely by its new password sharing policy and the ad-supported tier

-It posted record revenues, up 7.8% y/y and expects further acceleration in the fourth quarter

-It added 8.76 million member, bringing its user base to 247.15 million

Strategic Changes

The hardships of the past year forced the streaming giant to change key aspects of its business. It cracked down on password sharing, limiting access to one household and launched a cheaper ad-supported plan.

These are both crucial initiatives that give Netflix the ability to convert borrowers to paying members, offer a less expensive entry point to price-pinched consumers at a period of increased competition and provide an additional revenue stream from advertisers.

The beneficial impact of those strategic changes was evident in July's Q2 results, but Wednesday's latest report for the third quarter revealed further progress, driving a lift on both revenues and the user base.

Revenue Acceleration

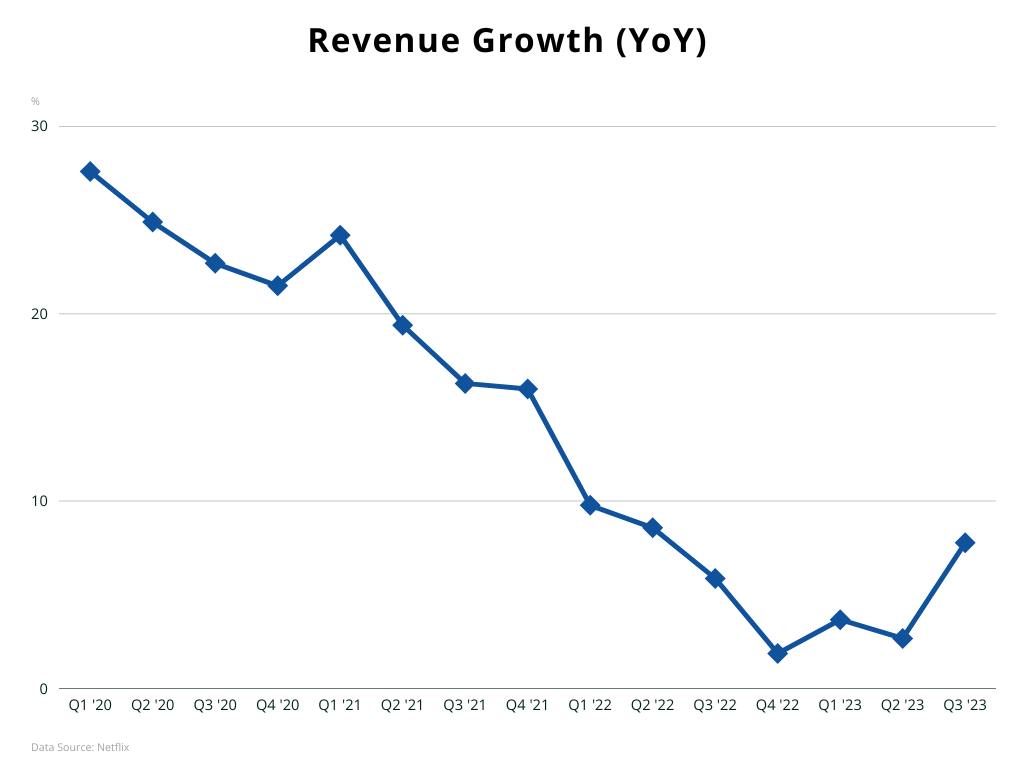

Netflix posted record revenues of 8.542 billion in the third quarter, in line with its own guidance [1]. Despite generally robust figures, the slow pace of increases has been concerning, with falling rates over the past two years.

Wednesday's figure though marked a substantial year-over-year growth of 7.8% y/y. Furthermore, the firm expects revenue growth to accelerate further in Q4, to 10.7% y/y. This would mark the first double-digit growth in two years.

The streaming leader noted that the recent results and latest forecast reflect the success of the new paid sharing policy and that it is "revenue positive in every region". Netflix did not expect the ad-supported tier to be a big contributor this year, but believes it will develop into a "multi-billion dollar revenue stream over time".

United States and Canada (UCAN) remained the largest contributors, with $3.735 billion and a slight increase sequentially and yearly. Despite the surge in sales, Average Revenue per User (ARM) was underwhelming. It dropped 1% y/y, partly due to "limited price increases over the past 18 months".

Its bottom line strengthened significantly, since net income jumped to $1.667 billion and the highest since the first quarter of 2021. Operating margins widened to 22.4%, from 22.3% in the previous quarter and 19.3% in Q3 2022.

User Base Expansion

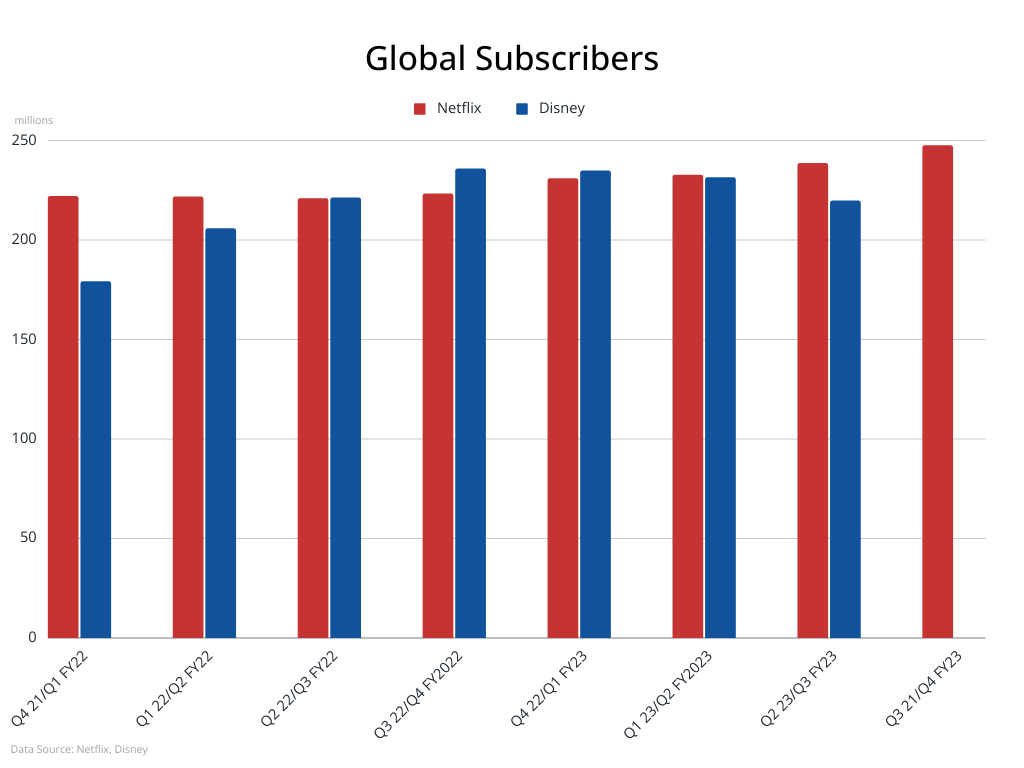

The firm had posted a shocking loss of around 1 million subscribers in the first half of 2022 and conceded the top-spot to Disney. However, it returned to growth in the ensuing quarters and was able to reclaim the lead, as its rival undergoes a challenging period and has been losing subscribers. Yesterday's report showed the addition 8.76 million paid members in Q3, bringing its total subscribers to 247.15.

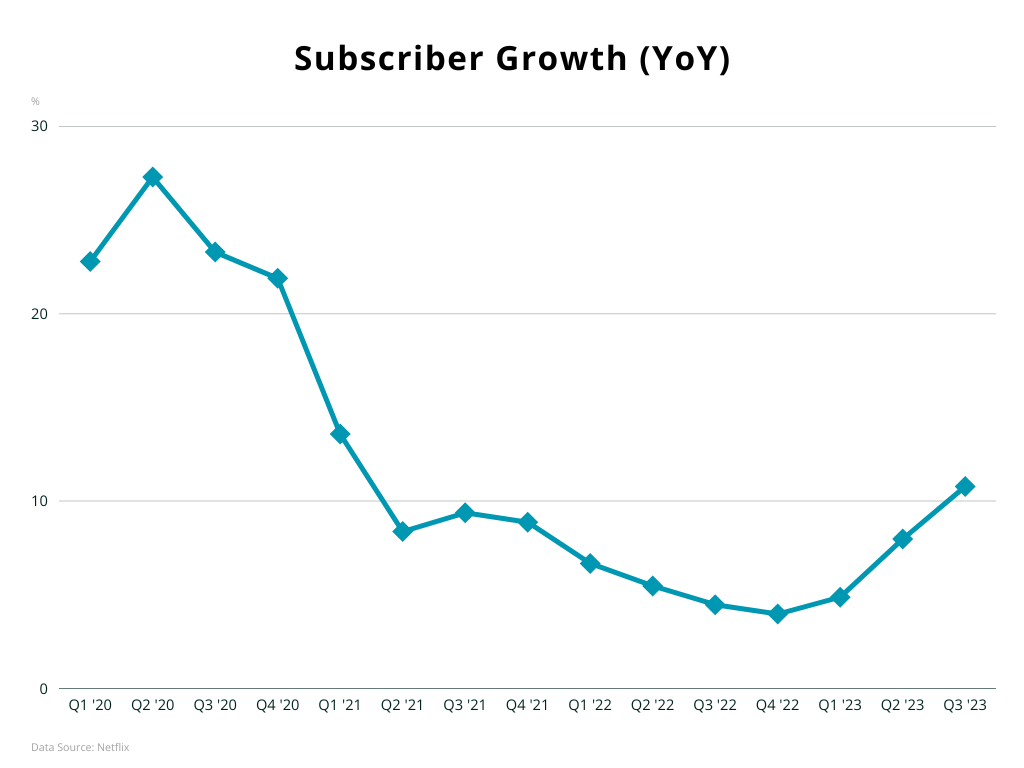

The pace of additions has been dropping since early 2021, but picked up again this year. The Q3 figures marked a return to double-digit growth for the first time in more than two years. Although they don't offer exact projections any longer, executives expect "similar" number of new members in the fourth quarter, which would lead to further acceleration in the rate of expansion of its user base.

Netflix highlighted that fact that the subscription plan that includes commercials registered a 70% q/q increase in memberships and now accounts for 30% of signups in the applicable countries. Executives also stood on the positive impact of the crackdown on password sharing, as borrowers convert to paying members and the cancel reaction "continues to be low". Netflix had previously estimated 100 million sharing households, so there is room for more conversions. During the earnings call, CFO Spencer Neumann said "we've got a long runway for growth" in both the user base and ARM. [2]

Price Hikes

Despite the substantial acceleration of revenue and subscriber growth, Netflix announced price hikes in the US, UK and France, to its Premium and Basic plans. The latter is already being phased out, in favor of the ad-supported tier, which is the cheapest and remained unaffected by the price increase ($6.99 in the US) and so did the Standard plan. The firm spoke of "extremely competitive" starting price.

Other streamers have also raised their prices over the past several months, with Disney being one of the most aggressive. It has kept the cost of its ad-supported plan unchanged though, trying to offer a low entry point that can potentially be more profitable, due to the revenues for advertisers. Netflix appears to be following a similar path to its archrival.

The recent negotiations with the writers and actors are likely one the drivers behind the increased prices, since they will likely lead to higher costs for the entertainment companies. Following the lengthy strikes, agreement between the industry and the Writers Guild (WGA) has been achieved, but not yet with the screen actors (SAG-AFTRA), who stay on the picket line. Netflix forecasts around $13 billion in content spend this year, assuming the dispute is resolved, but expects this cost to spike up to $17 billion in 2024.

Sports Content

The streaming giant does not host live sports, even though it is heavy on sports-adjacent content, having "great success" with its docuseries like Quarterback and Formula 1: Drive to Survive. Co-CEO Theodore Sarandos said that the firm is focusing on the part of the segment that it brings the most value to, which is "the drama of sport". [2]

However, Netflix is now making a timid step into live programming, with the one-off Netflix Cup golf competition, scheduled for mid-November [3]. Mr Sarandos noted that Netflix is "investing heavily in increasing" its live capabilities, but stressed that there are no core changes to its strategy. [2]

Netflix has many reasons to stay out of live sports, since this a challenging pursuit technically and securing licensing agreements is a messy and costly affair. This would be a difficult endeavor, as the streaming giant pushes on converting borrowers, on building its advertising business and other projects.

On the other hand, live sports is the next logical step after the entry into the advertising market, being naturally suited for inclusion of commercials, given half-times, viewer-engagement and other factors. It also has the potential to attract vast amount of users and drive revenue. According to Nielsen, Broadcast TV viewing rose 13% in September in the US, due to the return of college and professional football and viewing of sports programming soared 360%. Streaming usage meanwhile, declined for second month in a row. [4]

Furthermore, Netflix will have to eventually tap that market, in order to fend off increasing competitiom. Legacy entertainments giants like Disney and WarnerBros.Dicovery offer live sports. Tech behemoths like Amazon.com and Apple who make strides in streaming with their deep pockets, also have live sports events.

Conclusion

Markets have been cautious around Netflix over the past few months, despite the encouraging signs from its strategic initiatives, amidst broader underwhelming performance of the tech sector. Its stock lost around 15% of its value in the third quarter and drops further in the current month.

However, Wednesday's result showed that Netflix is a growth story again, with the acceleration in revenues and subscribers. Markets reacted positively and the stock was gaining more than 10% in Thursday's pre-market trading.

The streaming giant appears to be on the right path with the new ad-supported tier and the paid sharing policy, but remains to be seen how much runway there is left. It is pushing further into gaming and plans to open physical Netflix Houses to "deepen fandom" according Mr Sarandos [2]. Although these are not expected to have the scale of theme parks, they can help Netflix extrapolate its content into various channels, the way Disney and others do.

Everything seems to be going its way currently, but there are still challenges ahead. Legacy media powerhouses may struggle, but they have compelling content that Netflix could have a hard time to match, despite increasing reliance on third-party programs. Furthermore, the streaming market is getting saturated and consumers have many options, including free linear ad-inclusive streaming (known as FAST). At the same time, elevated inflation continues to create headwinds.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. He has a long time presence at FXCM, as he joined the company in 2011. He has served from multiple positions, but specializes in financial market analysis and commentary.

With his educational background in international relations, he emphasizes not only on Technical Analysis but also in Fundamental Analysis and Geopolitics – which have been having increasing impact on financial markets. He has longtime experience in market analysis and as a host of educational trading courses via online and in-person sessions and conferences.

References

| Retrieved 19 Oct 2023 https://s22.q4cdn.com/959853165/files/doc_financials/2023/q3/FINAL-Q3-23-Shareholder-Letter.pdf | |

| Retrieved 19 Oct 2023 https://www.youtube.com/watch | |

| Retrieved 19 Oct 2023 https://www.netflix.com/tudum/articles/netflix-cup-live-event-date-news | |

| Retrieved 28 Apr 2024 https://www.nielsen.com/insights/2023/sports-gave-broadcast-channels-a-second-straight-month-of-viewing-gains-in-september/ |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.