EUR/USD Drops on Poor PMIs, in the Aftermath of ECB’s Outsized Rate Hike

ECB Rate Lift-off

The European Central Bank (ECB) raised rates for the first time in more than a decade on Thursday, opting for a bolder 50 basis points move [1]. This was contrary to its previous guidance, which had clearly signaled to a 0.25% lift-off in July, but had hinted to larger adjustment in September.

However, the more aggressive outcome did not come as a surprise, since a Reuters report earlier in the week, had pointed to the potential of such an outcome.[2]

The main diver for the ECB's outsized rate lift-off is surging inflation, as Eurozone's headline CPI hit new record high in June, at 8.6% year-over-year. Despite this, the bank's rhetoric is not as aggressive as that of other major central banks and it does not sound as resolute on fighting inflation.

Recession Fears

The reason for this reserved stance is probably the fact that he European continent is much more exposed to the economic fallout of the war in Ukraine and dependent on Russian oil and gas, with ECB officials acknowledging the risks this poses to growth.

Gas from Nord Stream 1 may have begun flowing again yesterday after the ten-day maintenance shutdown, but fears that Russia cut-off supply remain elevated. [3]

The Euro's recent plunge to parity was largely triggered by poor European PMIs earlier in the month, while today's preliminary data for July don't paint a pretty picture either, sustaining recession fears.

Politics is another source of risk, since highly indebted Italy and one of the EU's largest economies is going through another political crisis, which pushes Italian bonds lower. Prime Minister Draghi resigned on Thursday and the country now heads towards snap elections.

Guidance Thrown Out of the Window

After yesterday's outsized move, the forward guidance on rates now seems to have been thrown out of the window, as the statement pointed to more rate normalization ahead, but the Governing Council will now follow a "meeting-by-meeting approach".

Furthermore, Ms Lagarde clearly stated during her press conference that the guidance that previously existed for September "is no longer applicable". She added that the bank is "accelerating the exit" but it is "not changing the ultimate point of arrival", although she had difficulty articulating what that level actually is. [4]

Stark Contrast with the Fed

The European Central bank stepped into the rate normalization trail, but the differential with the US Federal Reserve remains stark, since the latter has already delivered 150 basis points worth of hike.

Furthermore, its wording against inflation is much stronger and its resolve to bring it down far more pronounced, while it has also clearly communicated its intentions for a 0.5-0.75% hike at next week's meeting. [5]

Markets seem to be on board, as previous expectations for a bigger move have retreated, since Fed officials did not lose their cool after the latest inflation jump and stuck to the well-communicated plan.

However, the Fed's hawkishness may have peaked, since if does not go overboard this month with a full percentage point increase, it is hard to see doing so in the future.

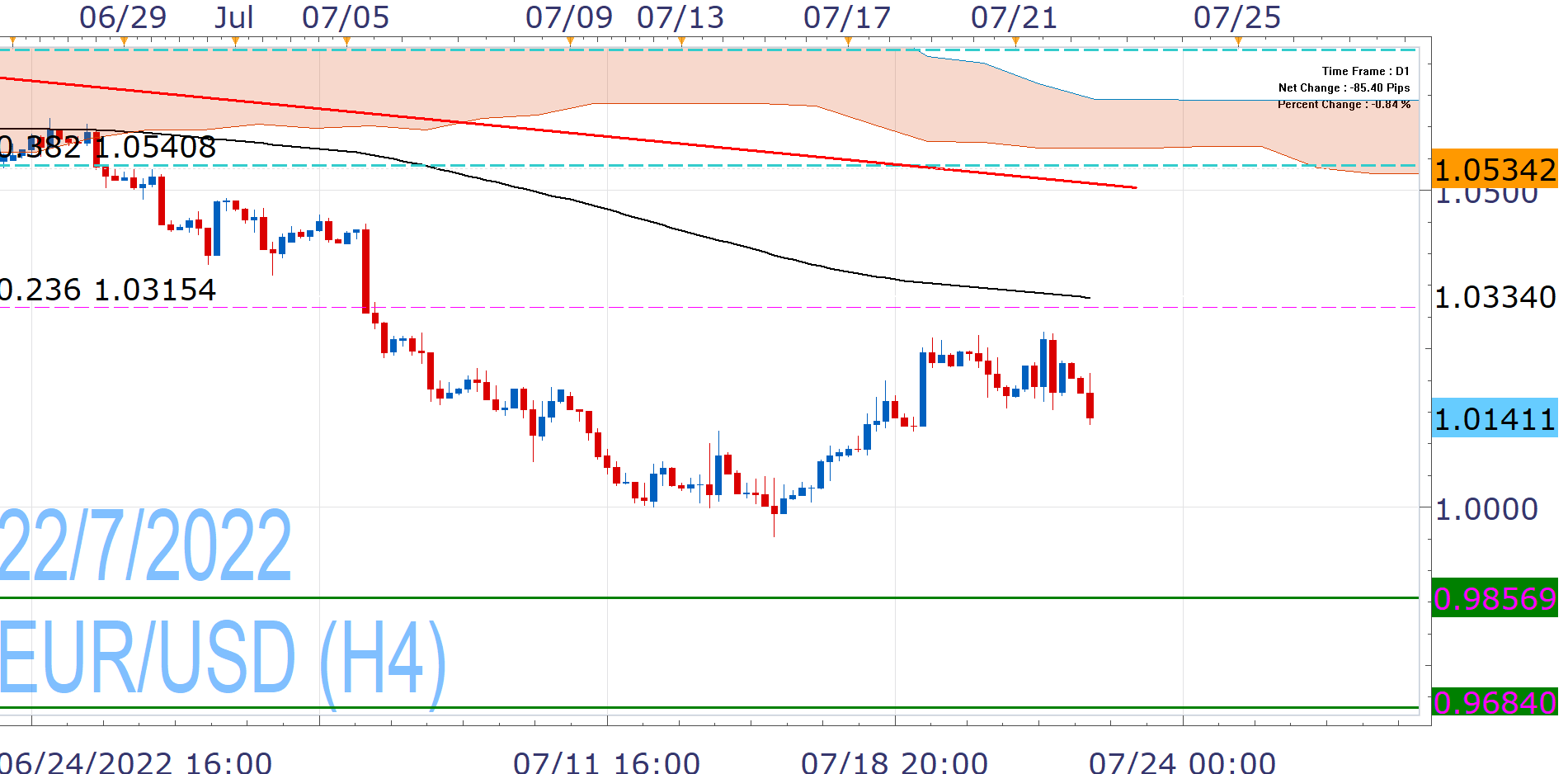

EUR/USD Analysis

The progression of this policy differential is what will likely determine the pair's trajectory and market will be keenly awaiting the Fed July 27 decision and its intentions regarding the next meeting in September.

EUR/USD ended Thursday with profits, but erased much of its gains after Ms Lagarde's reference on the guidance for September.

Today's PMIs showed a drop to contraction territory for Germany's and Eurozone's manufacturing activity, which aggravates recession fears and sends the common currency lower. As such, it is still in risk of a reutrn to parity, although it may be early to talk of a breach of 0.9856.

The recent rebound of EUR/USD has given it the opportunity to challenge 1.0315-33, which is the critical 23.8% Fibonacci of the 2022 High/Low drop and the EMA200.

So far it has failed to do so and we are not optimistic about its broader ascending prospects, although a break above this level, could open the door to recovery towards the next Fibonacci and the descending trendline from this year's high (1.0500-40)

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. He has a long time presence at FXCM, as he joined the company in 2011. He has served from multiple positions, but specializes in financial market analysis and commentary.

With his educational background in international relations, he emphasizes not only on Technical Analysis but also in Fundamental Analysis and Geopolitics – which have been having increasing impact on financial markets. He has longtime experience in market analysis and as a host of educational trading courses via online and in-person sessions and conferences.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.