The US Fed Delivered Its Biggest Rate Increase in More than 20 Years

Biggest Hike in 2 Decades & Balance Sheet Reduction

The US Federal Reserve decided unanimously on Wednesday to increase interest rates by 50 basis points, to 0.75%-1.00%, as was largely expected. This was the second straight increase after the March lift-off and constituted the biggest hike since 2000 and the dot-com bubble.

The accompanying policy statement pointed to more adjustments ahead, as the Committee "anticipates that ongoing increases in the target range will be appropriate". [1]

The central bank had concluded its asset purchases program in March - which has inflated its balance sheet to nearly $9 trillion - and yesterday it announced a plan to reduce it.

The Fed will begin reducing its securities holdings in June 1, by $47.5 billion/month for three months. This will include $30 billion/per month of Treasury Securities and $17.5 billion/month agency debt and agency mortgage-backed securities. After three months, these caps will increase to $60 billion/month and $35 billion/month respectively. [2]

Inflation Drives Tightening

The Federal Reserve had long viewed high inflation as transitory, focusing more on restoring the labor market, but was forced to change tack and embarked on an aggressive monetary tightening path in order to bring inflation down. On Wednesday, it reiterated its focus on this task, noting "The Committee is highly attentive to inflation risks", while recognizing that "Inflation remains elevated".

Chair Powell opened his press conference – the first in-person one since the pandemic – by addressing the American people directly and said that "Inflation is much too high", before adding that "We have both the tools we need and the resolve it". [3]

The Fed's preferred measure of Inflation, the Core Personal Consumption Expenditures which excludes food and energy prices moderated to 5.2% in March (year-over-year) from 5.3% prior (revised), while the inclusive headline PCE rose to 6.6% year-over-year, from 6.3% prior (revised).

Future Rate Adjustments

Mr Powell was forceful in his inflation messaging and the pledge to bring it down and restore price stability, but his comments around the bank's future moves were rather conservative.

During his press conference, he talked of "a broad sense on the Committee" that half-percentage point increases "would be on the table at the next two meetings", pouring cold water to the expectations of proponents of more aggressive hikes.

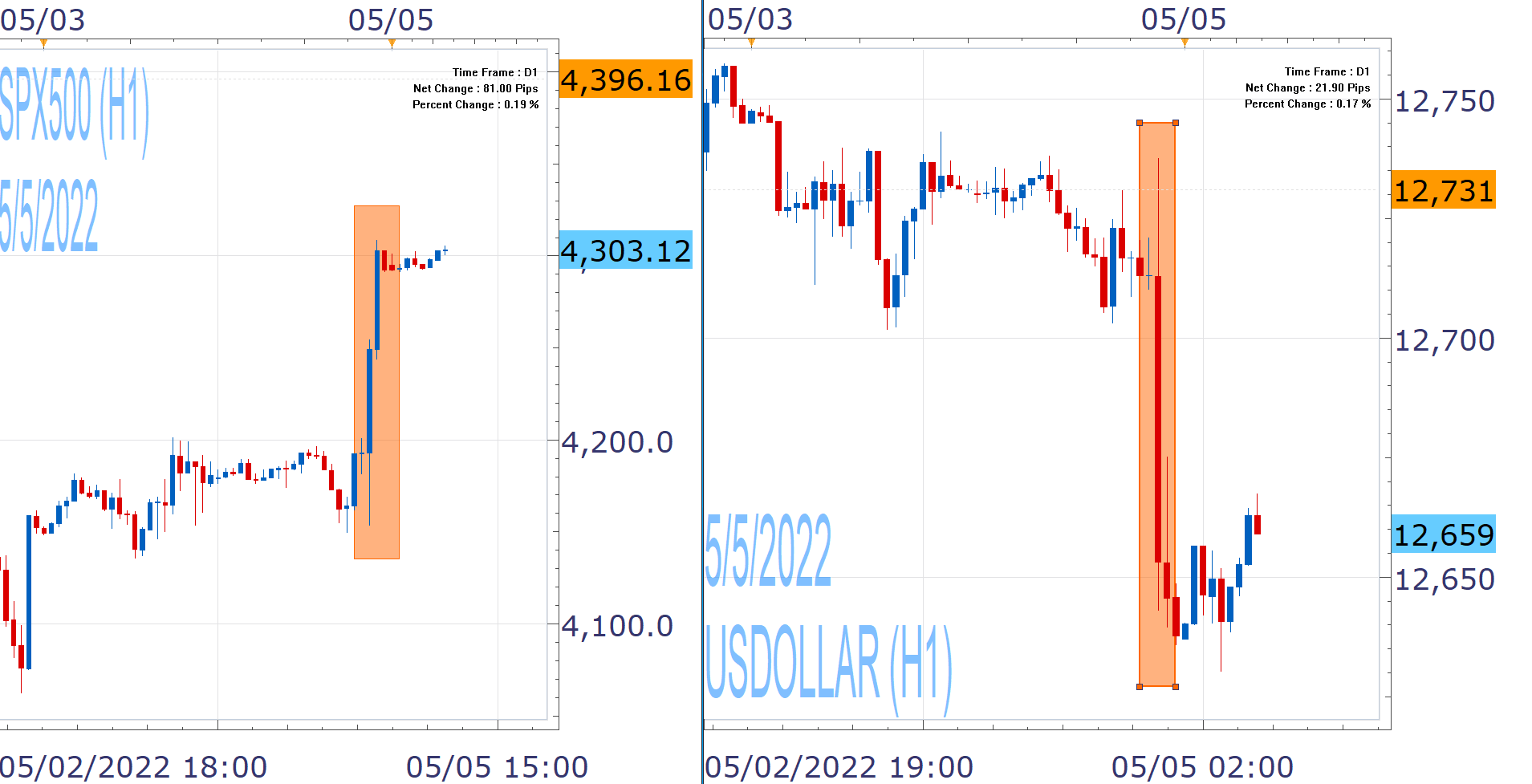

When asked around the size of upcoming adjustments, the Chairman said that 75 basis points increases is "not something the Committee is actively considering", which sent the US Dollar lower and US equities higher.

Economic Activity & Labor Market

Last week's preliminary data revealed that the US economy contracted in the first quarter of the year, as advance annualized Q1 GPD was -1.4%, from 6.9% final reading for Q4 2021.

Yesterday the bank acknowledged that the economic activity "edged down in the first quarter", citing "highly uncertain" implications from the war in Ukraine, which are "likely to weigh" on the economy.

The latest employment report is due on Friday, but the last data showed that Unemployment dropped to 3.6% in March, 431,000 new jobs were added and the participation rate ticked up to 62.4%.

Recent data have been supportive of the Fed's tightening, which said yesterday that "job gains have been robust in recent months, and the unemployment rate has declined substantially", while Chair Powell reiterated that the labor market is "extremely tight".

The big question now is whether the Fed can bring down inflation without plunging the economy into a recession and causing another surge in unemployment. This is definitely not an easy task and Mr Powell's reference of achieving a "soft or softish landing" did not inspire much confidence.

Market Reaction

The Federal Reserve has done a good job in communicating its actions well in advance, having prepared markets for the 50 basis point interest rate increase and the balance sheet runoff.

As such, US stock markets were relived from the lack of any hawkish surprise and the fact that Mr Powell pretty much ruled out bigger hikes sent them higher and the US Dollar lower.

Despite some dovishness in the bank's rhetoric, the reality remains that it is on an aggressive and front-loaded monetary tightening path, and far ahead than most of it major counterparts, despite recent hawkish shift form some of them, such as the Reserve Bank of Australia.

Nikos Tzabouras

Senior Financial Editorial Writer

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. He has a long time presence at FXCM, as he joined the company in 2011. He has served from multiple positions, but specializes in financial market analysis and commentary.

With his educational background in international relations, he emphasizes not only on Technical Analysis but also in Fundamental Analysis and Geopolitics – which have been having increasing impact on financial markets. He has longtime experience in market analysis and as a host of educational trading courses via online and in-person sessions and conferences.

References

| Retrieved 05 May 2022 https://www.federalreserve.gov/newsevents/pressreleases/monetary20220504a.htm | |

| Retrieved 05 May 2022 https://www.federalreserve.gov/newsevents/pressreleases/monetary20220504b.htm | |

| Retrieved 25 Apr 2024 https://www.youtube.com/watch |

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.