The RBA Response to Covid Supported Employment

Australian Unemployment and the RBA's Response During the Covid Pandemic

The Reserve Bank of Australia or RBA is Australia's central bank. It is the custodian of the country's monetary policy and aims to contribute to:

- The stability of the currency of Australia;

- The maintenance of full employment in Australia; and

- The economic prosperity and welfare of the people of Australia.

As the central bank decides on and institutes its various policy decision, it will do so in reference to these obligations. It has independence in exercising policy as it sees fit but is accountable to Parliament for its actions. In this article, we focus on unemployment and how the RBA's response during the covid pandemic period contributed to achieving its second mandate.

The Covid-19 Pandemic and Australia's Labour Market.

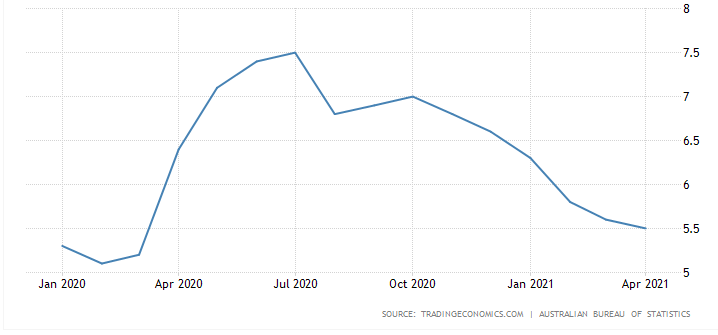

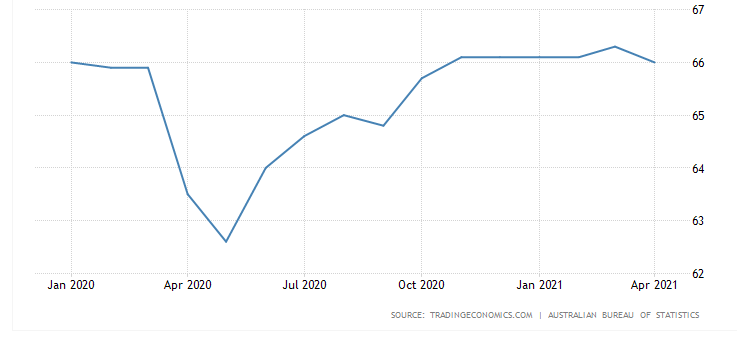

As the covid pandemic spread globally, regional economies were severely affected as lockdowns took hold and business and consumer confidence levels fell sharply. Prior to this period, Australia's unemployment rate was around the 5.2% mark with a labour participation rate of 65.9%. However, as the global lockdown period progressed, taking its toll on economic activity, the labour statistics deteriorated considerably. By May the labour force participation rate had dropped to 62.6% and unemployment had climbed above 7%.

The RBA's Monetary Policy Response to Support the Economy

The RBA countered the economic shocks caused by the covid pandemic in a number of ways, ensuring a comprehensive and effective response that provided support to jobs, incomes and business:

- The RBA adjusted its policy interest rate by lowering the cash rate twice. First to 0.25% in March 2020 and then to 0.1% in November 2020. This aimed for easier borrowing and spending confidence.

- Forward guidance was emphasised, and the RBA has stated that the cash rate will only be adjusted when actual inflation falls within the 2-3% target range, which is expected in 2024. This has increased certainty regarding the economic outlook.

- The 3-year bond has a targeted yield of 0.1% and the RBA will provide the demand so that this is achieved. Moreover, the central bank is purchasing 5- and 10-year bonds as part of its quantitative easing effort. This helps keep a lower yield across the yield curve, which is supportive of expansion, through easier borrowings and spending confidence across longer times frames.

- The RBA also extended favourable term funding to commercial banks at a rate of 0.1%. These borrowings are able to be passed on as loans to business and households. This is regarded as especially important to support the liquidity requirements of small- and medium sized businesses.

- Lastly, the central bank ensured a floor under the cash rate by implementing zero interest on Exchange Settlement balances. This in turn put a floor under all rates.

The RBA Statement of 1 June 2021

Whilst monetary policy was not Australia' only response to the pandemic, it certainly may be regarded as a strong response and largely successful in terms of supporting Australia's unemployment rate. In its statement dated 1 June 2021 the following paragraph is noteworthy:

"Progress in reducing unemployment has been faster than expected, with the unemployment rate declining to 5.5 per cent in April. Job vacancies are at a high level and a further decline in the unemployment rate to around 5 per cent is expected by the end of this year. There are reports of labour shortages in some parts of the economy."

To conclude this article, consider the line charts of Australia's unemployment rate (top chart) and participation rate (bottom chart) from 1 January 2020 until the present as a testament to the RBA and its policy response to the Covid pandemic.

Russell Shor

Senior Market Specialist

Russell Shor joined FXCM in October 2017 as a Senior Market Specialist. He is a certified FMVA® and has an Honours Degree in Economics from the University of South Africa. Russell is a full member of the Society of Technical Analysts in the United Kingdom. With over 20 years of financial markets experience, his analysis is of a high standard and quality.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.