Consumer Sentiment Hit By Inflation Concerns

In this article:

1. University of Michigan consumer survey misses consensus.

2. US consumers are gloomy.

3. Inflation is rampant.

4. The Fed may have to pivot on policy.

Friday's preliminary consumer sentiment reading from the Univesity of Michigan was sobering. US consumers are hurting. Last month's print was 71.7, and 72.5 was the consensus for Friday's number - it came in at a paltry 66.8. Faced with the prospects of longer and broader inflation, consumers are despondent. Earlier in the week, headline CPI, at 6.2% y/y, inferred the steepest inflation reported in 31 years. This is reflected in consumer confidence, now at its lowest level in a decade. Previously, we suggested that the Fed may be behind the curve in terms of monetary policy. In our estimate, the Fed has reached a ceiling on how far it can continue with its view of "transitory" inflation. In other words, a pivot in policy has become probable.

Past performance is not an indicator of future results

Source: www.tradingview.com

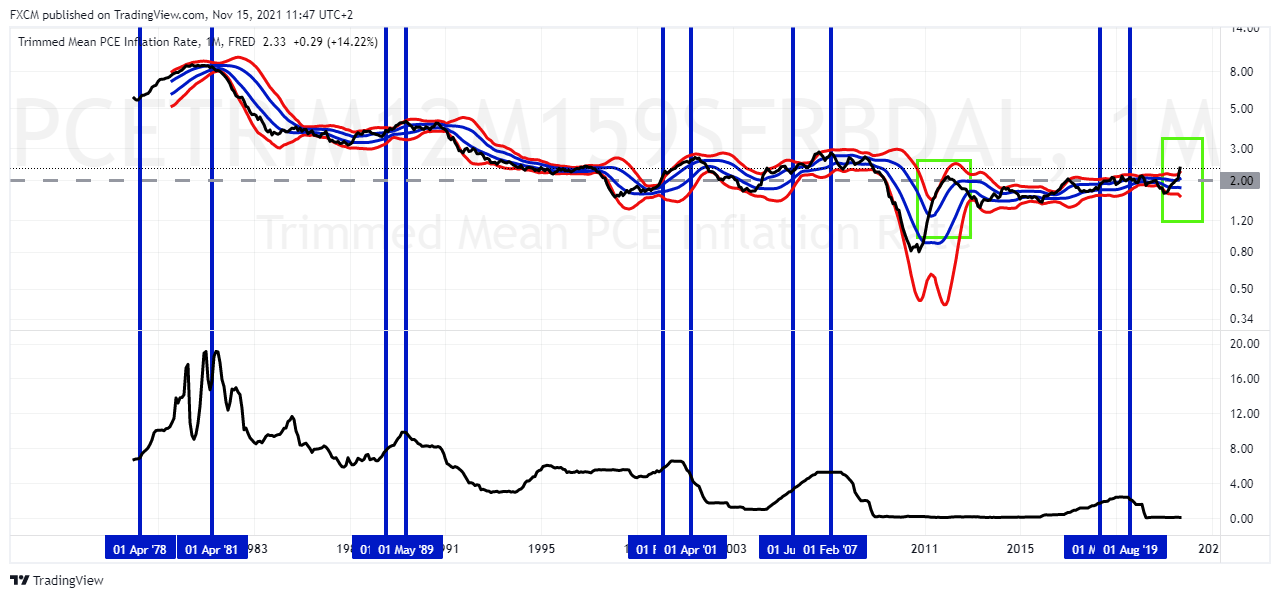

In this chart we consider the Dallas Fed's trimmed mean PCE. It is a good gauge of core inflation as outliers have been discarded in its calculation. Our interpretation is based on the red and blue Bollingers and the lower chart, which is the fed funds rate. Whenever the trimmed mean PCE moved into the area of strength (upper blue and upper red bands), the fed usually reacted - as can be seen by the increase in the fed funds rate (blue verticals).

Of note, this did not happen after the GFC (first green rectangle). Here, the Fed allowed for inflation to normalise and it did. The difference this time is the level of the trimmed mean PCE. We have drawn a dashed gray line at 2%, which is referenced as a target for the Fed's price stability mandate. We do acknowledge the change announced in August 2020, where the 2% was changed from an absolute target to an average target. However, the trimmed mean has already discarded outliers, which suggests that the Fed is very close to where it wants to be. The current reading is 2.33%. Given this, unless there is a certain retraction in inflation in the near- to mid-term, the Fed will need to seriously consider a pivot in its current monetary policy.

Russell Shor

Senior Market Specialist

Russell Shor joined FXCM in October 2017 as a Senior Market Specialist. He is a certified FMVA® and has an Honours Degree in Economics from the University of South Africa. Russell is a full member of the Society of Technical Analysts in the United Kingdom. With over 20 years of financial markets experience, his analysis is of a high standard and quality.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interests arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed here.